Published by CR Equity AI | June 2026 | crequity.ai/aivaa

The mortgage industry has a velocity problem. Borrowers expect home equity lines of credit approved in minutes and funded in days. Capital markets demand blockchain-verified collateral data in real time. Yet the traditional appraisal — the cornerstone of collateral protection since the inception of modern mortgage lending — still takes three to six weeks to complete in many markets. For mortgage note buyers, mortgage loan originators (MLOs), private brokerages, private offices, and private equity firms deploying capital into residential and non-QM lending, that gap between expectation and execution is no longer a minor inconvenience. It is a structural competitive disadvantage.

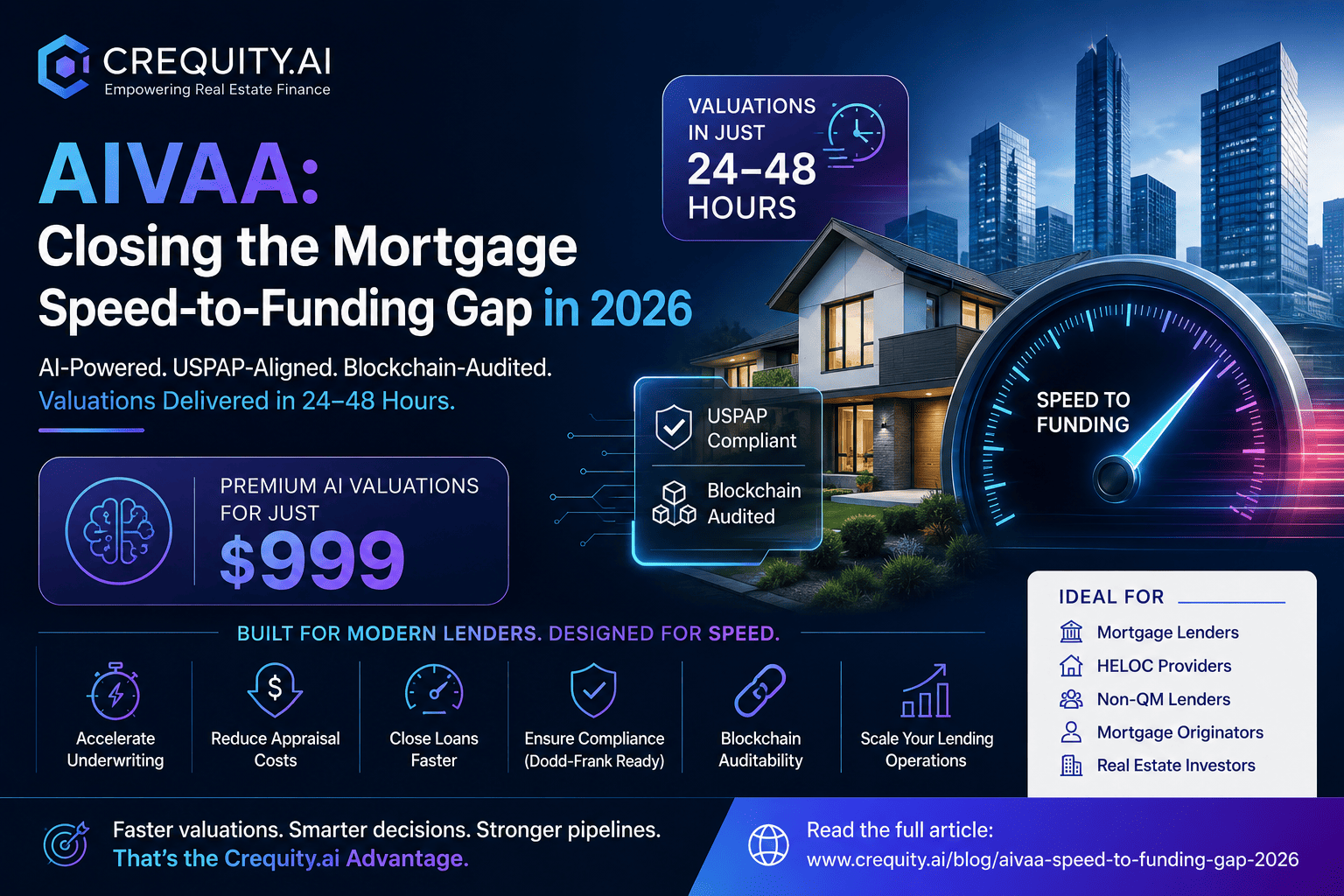

AIVAA (AI Valuation Agent & Analysis), the flagship platform from CR Equity AI, is engineered to close that gap. By delivering a comprehensive, USPAP-aligned, blockchain-audited property valuation in 24–48 hours at a flat fee of $999, AIVAA operates as a parallel rail alongside the underwriting process — not as a sequential bottleneck before it. The result is a loan cycle measured in days rather than weeks, with no sacrifice of regulatory compliance, audit trail integrity, or collateral protection quality.

The Market Forces Making AI Valuation Unavoidable

The urgency behind AI-native valuation is not a technology trend story. It is a convergence of three structural market forces that are simultaneously squeezing traditional appraisal workflows from every direction.

The appraiser supply crisis is accelerating. The total number of active residential appraisers completing field work in the United States has been declining steadily for years, and the profession faces a demographic collapse as a disproportionate share of its workforce approaches retirement age. The pipeline of new entrants remains thin despite industry efforts to streamline certification pathways. During periods of elevated origination volume — such as the HELOC boom currently underway — appraisal turn times in many markets extend well beyond the industry standard of five to seven business days, with complex or rural properties routinely taking three to six weeks. For lenders competing on speed-to-funding as a primary differentiator, this creates a fundamental bottleneck that no amount of process optimization can resolve without addressing the underlying supply constraint.11

The HELOC boom is rewriting competitive expectations. American homeowners held approximately $11.5 trillion in tappable home equity as of early 2025, yet only 0.41% of that equity was accessed in Q1 2025 — representing an enormous latent demand pool.21 Home equity originations increased 14.3% year-over-year in Q3 2025, HELOC balances grew by approximately $11 billion in the same quarter to roughly $422 billion, and the U.S. home equity lending market is projected to reach $220.88 billion by 2030 at a CAGR of 4.27%.7 The competitive landscape has been transformed by digital-native lenders who have made speed-to-funding a primary differentiator — with the leading fast-HELOC lenders in 2026 offering approval timelines measured in minutes and funding timelines measured in days. The enabling technology behind this speed compression is, in virtually every case, the replacement of traditional in-person appraisals with automated valuation models.

The regulatory environment has raised the floor, not the ceiling. The Dodd-Frank AVM Final Rule, effective October 2025 and jointly issued by the OCC, Federal Reserve, FDIC, NCUA, CFPB, and FHFA, implements quality control standards for automated valuation models used in credit decisions.3 The rule does not restrict AVM usage — it standardizes quality control requirements, effectively creating a compliance framework that legitimizes AVM deployment for a broader range of credit decisions. Lenders who deploy AVM solutions with built-in compliance documentation, audit trails, and fair lending screening are positioned to satisfy the rule’s requirements more efficiently than those relying on basic AVM subscriptions that require separate compliance infrastructure.

The global AVM market reflects this momentum: valued at approximately $4.2 billion in 2024, it is forecast to reach $11.5 billion by 2033 at a CAGR of 11.7%.1 The broader AI-in-real-estate segment is forecast to reach $1.3 trillion by 2030.2 These are not speculative projections; they are grounded in live market dynamics already reshaping how capital is deployed across the mortgage stack.

What AIVAA Delivers — and Why It Matters to Every Participant in the Lending Stack

AIVAA is not a commodity AVM subscription. It is an institutional-grade valuation platform that combines machine learning valuation, a blockchain-verified audit trail, confidence scoring, SHAP explainability, and a comprehensive compliance framework aligned with the Dodd-Frank AVM Final Rule, SR 11-7 Model Risk Management guidance, USPAP Advisory Opinion standards, and ECOA/Regulation B. The distinction matters enormously for every participant in the mortgage lending ecosystem.

For Mortgage Note Buyers

Mortgage note buyers acquiring performing and non-performing residential and commercial notes face a persistent challenge: the collateral documentation supporting the notes they purchase is often inadequate for secondary market resale, portfolio reporting, or litigation defense. A basic AVM output — a PDF with a point-in-time value estimate and a confidence score — does not provide the audit trail, methodology documentation, or regulatory compliance attestation required to defend that valuation in the event of a default, repurchase demand, or regulatory examination.

AIVAA addresses this gap by providing documentation depth equivalent to a traditional appraisal — three simultaneous valuation approaches (Income, Sales Comparison, and Cost), a reconciliation narrative, a confidence score with Forecast Standard Deviation (FSD), a SHAP explainability report, and a blockchain-verified chain of custody — at the speed and cost profile of an AVM. For note buyers evaluating large pools of collateral on compressed timelines, AIVAA’s ability to process unlimited concurrent orders at $999 per valuation versus $3,500–$15,000 for a traditional MAI appraisal represents a transformative reduction in due diligence cost and timeline.

For Mortgage Loan Originators and Brokerages

MLOs and brokerages competing in the fast-HELOC and non-QM origination market face a dual pressure: borrowers demand speed, and investors demand documentation. The leading fast-HELOC lenders in 2026 offer five-minute approvals and five-day funding — a standard that is impossible to achieve with a three-to-six-week appraisal in the workflow.8

AIVAA’s parallel rail architecture resolves this tension directly. Because AIVAA can complete a comprehensive valuation in 24–48 hours — and because the platform’s data ingestion, market analysis, and ML modeling can begin the moment a property address is submitted — the valuation process runs concurrently with credit analysis, income verification, and title search rather than sequentially after them. The result is a clear-to-close timeline compressed from 15 days to 10 days per loan, returning five days to the pipeline on every transaction. At a monthly origination volume of $50 million with a 25% AIVAA deployment share and an average loan size of $400,000, this translates to approximately 625 loan-days saved per month — or roughly 7,500 loan-days per year.

For brokerages managing high-volume pipelines, the cost savings compound quickly. At $750 in displaced appraisal fees per loan, a brokerage originating 125 AIVAA-valued loans per month saves $93,750 monthly — approximately $1.125 million over 12 months at a $400,000 average loan size, and approximately $1.5 million at a $300,000 average loan size.

For Private Offices and Private Equity

Private offices and private equity firms deploying capital into residential mortgage, non-QM, and home equity lending face a collateral documentation challenge that is structurally different from that of institutional lenders. Without GSE backing, every loan in a private capital portfolio must stand on the quality of its own collateral documentation. Warehouse lenders, secondary market investors, and co-investment partners all require verifiable, audit-ready collateral assessments — and the absence of a documented audit trail creates repurchase risk that can materially impair portfolio economics.

AIVAA’s blockchain audit trail is particularly significant in this context. Every AIVAA valuation is cryptographically signed and immutably recorded on a blockchain ledger, timestamped and hash-verified from data ingestion through final value conclusion. This five-stage ledger process — Capture, Engine, Seal, Ledger, Access — creates a tamper-evident chain of custody that satisfies the AVM Final Rule’s data integrity requirements, supports appraisal-independence documentation, and provides secondary market participants and warehouse lenders with a verifiable record of the valuation process.

For private equity firms exploring tokenized mortgage instruments — a market that surged over 100% in the first half of 2025 alone, reaching approximately $20 billion in tokenized real-world assets — the blockchain audit trail is not merely a compliance feature. It is essential infrastructure. When a mortgage is tokenized and its tokens trade on secondary markets, the loan-to-value ratio of the underlying collateral must be continuously verifiable to support accurate pricing. Smart contracts governing payment distribution, covenant compliance, and margin calls require real-time or near-real-time access to property valuation data. AIVAA’s blockchain-verified architecture is compatible with the collateral verification requirements of blockchain-based capital markets infrastructure — a capability that standard AVM providers do not offer.20

The Confidence Scoring Cascade: Risk-Tiered Valuation for Every Asset Type

One of AIVAA’s most operationally significant features is its confidence scoring system, which produces a quantitative assessment of valuation reliability on a 0–100 scale alongside a Forecast Standard Deviation (FSD %) and Hit Rate Probability (within ±10% of market). These metrics drive a cascade decision matrix that determines the appropriate level of human oversight for each valuation:

| Confidence Score | FSD | Required Action |

|---|---|---|

| ≥ 80 | ≤ 12% | AIVAA-only report accepted |

| 65–79 | 12–17% | AIVAA Hybrid: desk review by licensed appraiser required |

| < 65 | > 17% | Full URAR appraisal required; AIVAA process suspended |

This cascade architecture is precisely the kind of risk-based, tiered approach that regulators and secondary market investors expect from an institutional-grade valuation program. It ensures that AI is used where it is most reliable and that human judgment is invoked where uncertainty is elevated — satisfying both the speed requirements of digital lending and the oversight requirements of the regulatory framework. For non-QM lenders operating in a segment where loans must be sold to private capital markets or held on warehouse lines with their own collateral quality requirements, this tiered approach provides the documentation depth of a traditional appraisal at the speed and cost profile of an AVM.

AIVAA vs. the Alternatives: A Direct Comparison

The competitive landscape for property valuation in 2026 offers three primary options: traditional MAI appraisals, commodity AVM subscriptions, and institutional-grade AI valuation platforms like AIVAA. The differences are not marginal.

| Criteria | AIVAA (CR Equity AI) | Traditional MAI Appraisal | Standard AVM |

|---|---|---|---|

| Turnaround Time | 24–48 hours | 3–6 weeks | Minutes (no inspection) |

| Cost per Valuation | $999 flat fee | $3,500–$15,000+ | $50–$200 (subscription) |

| Methodology | ML + Income + Sales + Cost (simultaneous) | Single appraiser judgment | Statistical model only |

| Market Data Currency | Real-time feeds | Point-in-time at inspection | Varies (often lagged) |

| Scalability | Unlimited concurrent orders | Limited by appraiser capacity | High |

| Audit Trail | Blockchain-verified, immutable | PDF report, no chain of custody | Typically absent |

| Regulatory Compliance | Built-in AVM Final Rule compliance | USPAP-compliant (when certified) | Requires separate QC framework |

| Confidence Scoring | Granular (score + FSD + hit rate) | Appraiser judgment | Basic (if provided) |

| Fair Lending Screening | SHAP proxy variable clearance | Appraiser-dependent | Typically absent |

| Cascade Decision Logic | Automated (AIVAA → Hybrid → Full) | Manual | Manual |

The traditional MAI appraisal remains the gold standard for complex, high-value, or contested properties — and AIVAA’s cascade architecture is designed to route those properties to licensed appraiser review. But for the high-volume, time-sensitive origination workflows that define the HELOC, non-QM, and note acquisition markets in 2026, the traditional appraisal’s three-to-six-week timeline and $3,500–$15,000 cost structure are operationally disqualifying. The commodity AVM, meanwhile, provides speed but lacks the audit trail, compliance documentation, and methodology depth required for institutional-grade collateral protection.

AIVAA occupies the institutional middle ground: the speed and scalability of an AVM, the documentation depth and compliance rigor of a traditional appraisal, and the blockchain-verified audit trail required for tokenized capital markets.

The Warehouse Line Velocity Multiplier

For warehouse lenders and the originators who rely on them, the financial case for AI-native valuation extends well beyond appraisal fee savings. Warehouse lenders advance funds against individual loans and are repaid when those loans are sold to secondary market investors. The longer a loan sits on the warehouse line, the higher the carrying cost and the lower the effective yield on the warehouse facility. Every day saved in the loan cycle directly improves the economics of the warehouse relationship for both the lender and the warehouse provider.

At a base case of 125 AIVAA-valued loans per month at $400,000 average loan size, the five days saved per loan represents 625 loan-days of warehouse line exposure eliminated each month. Over a 12-month period, this translates to approximately 7,500 loan-days of improved warehouse velocity, with compounding benefits as faster note sell-off enables more origination volume on the same warehouse line capacity. The velocity benefit — faster warehouse line turns, accelerated note sell-off, improved capital efficiency — compounds over time in ways that the direct cost savings alone do not capture.

Warehouse facilities that incorporate AI valuation platform compliance into their due diligence and advance rate frameworks are positioned to align facility pricing with the actual risk and velocity profile of their borrowers’ operations — a structural advantage as the market bifurcates between lenders using institutional-grade valuation infrastructure and those relying on undocumented AVM subscriptions.

The Regulatory Imperative: Why “Good Enough” Is No Longer Good Enough

The Dodd-Frank AVM Final Rule has effectively raised the floor for AVM deployment across the industry. Lenders who were previously using basic AVM tools without formal quality control documentation are now exposed to examination risk if they cannot demonstrate compliance with the rule’s five quality control factors: confidence in estimates, data integrity protection, conflict of interest avoidance, random sample testing and reviews, and compliance with applicable nondiscrimination laws.3

AIVAA was designed from the ground up to operate within this regulatory environment. The platform’s compliance framework is a seven-phase, step-by-step procedure that addresses every element of the AVM Final Rule, including pre-order eligibility screening, data validation, confidence score review, fair lending screening with SHAP proxy variable clearance, and regulatory framework attestation. The Quality Assurance framework establishes a comprehensive model governance structure covering pre-funding QC, post-closing QC, override tracking, and continuous model monitoring — satisfying the SR 11-7 model risk management requirements that apply to AI-driven credit decisions.

For non-QM lenders, private offices, and private equity firms operating outside the GSE framework, the compliance imperative is even more acute. Non-QM investors typically require more rigorous documentation of collateral quality than GSE loans, precisely because the absence of GSE backing means the investor bears the full collateral risk. The combination of high CLTVs, non-QM borrower profiles, and the “no in-person appraisal” feature that defines the fastest-growing HELOC products creates a collateral documentation challenge that a basic AVM cannot adequately address. AIVAA can.

Five-Year Outlook: The Window to Lead Is Now

The five-year outlook for the AVM and AI valuation market is one of accelerating adoption, rising regulatory standards, and growing integration with tokenized capital market infrastructure. The global AVM market is projected to nearly triple from approximately $4.2 billion in 2024 to $11.5 billion by 2033.1 The PropTech sector, within which AI valuation tools are embedded, is projected to expand from $44.59 billion in 2026 to $104.57 billion by 2034.6 The tokenized real estate market is expected to grow from hundreds of billions to trillions of dollars over the same period, with blockchain-verified collateral data becoming a standard feature of institutional-grade mortgage token infrastructure.15

The institutions that establish AI-native valuation capabilities now — before the tokenization wave fully arrives and before the appraiser supply crisis reaches its most acute phase — will be positioned to lead in the next generation of mortgage and home equity lending. The competitive differentiator over this period will not be AVM accuracy alone; most mature AVM providers have achieved acceptable accuracy within defined market conditions. The differentiator will be the ability to deliver audit-ready, regulatory-compliant, blockchain-verified valuations at the speed and scale required by modern capital deployment workflows.

That is the capability gap AIVAA is built to fill.

Who Should Be Talking to CR Equity AI Right Now

The AIVAA platform is purpose-built for the following participants in the mortgage and private capital ecosystem:

Mortgage note buyers acquiring performing, sub-performing, or non-performing residential and commercial notes who need institutional-grade collateral documentation at scale, on compressed due diligence timelines, and at a cost structure that preserves acquisition economics.

Mortgage loan originators and brokerages competing in the fast-HELOC, non-QM, and home equity origination market who need to compress clear-to-close timelines, reduce appraisal costs, and deliver the documentation depth that warehouse lenders and secondary market investors require.

Private offices managing family office capital, high-net-worth investor capital, or proprietary lending portfolios in residential mortgage, non-QM, and home equity who need a valuation solution that satisfies both the speed requirements of private capital deployment and the compliance requirements of institutional-grade collateral protection.

Private equity firms deploying capital into mortgage origination platforms, note portfolios, or tokenized mortgage instruments who need blockchain-verified collateral data that is compatible with smart contract infrastructure, secondary market due diligence, and regulatory examination.

Warehouse lenders and facility providers who want to align advance rate decisions and facility pricing with the actual risk and velocity profile of their borrowers’ valuation infrastructure.

The financial case is compelling. The regulatory case is clear. The competitive case is urgent. The mortgage industry’s speed-to-funding gap is closing — and AIVAA is the infrastructure making it possible.

Learn more about AIVAA — the AI Valuation Agent & Analysis platform from CR Equity AI.