7 min read

Foreign capital has always wanted a seat at the U.S. commercial real estate table. The appetite was never the constraint. What held it back was friction — unfamiliar rules, slow onboarding, and the difficulty of underwriting an asset from the other side of the world. That friction is now being dismantled by automation, and the timing matters, because cross-border money is moving again.

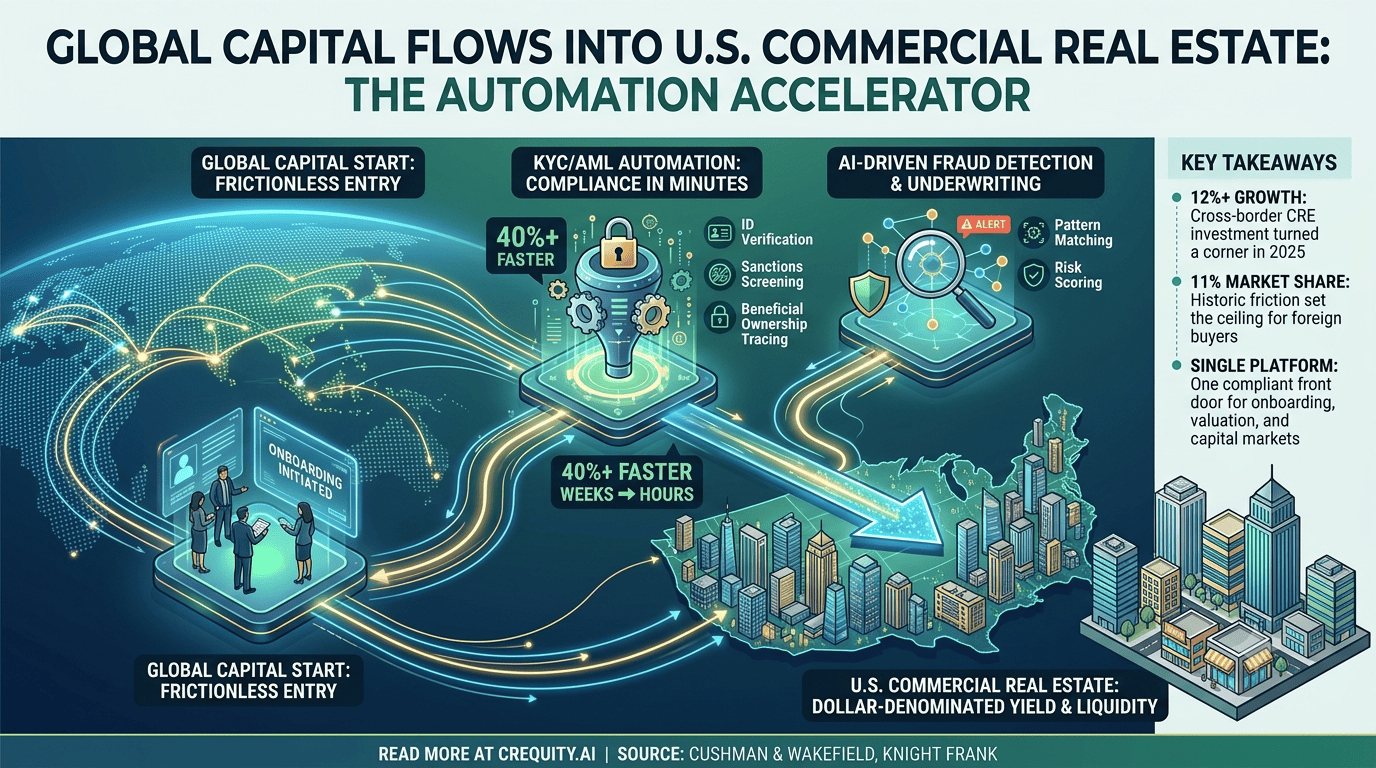

Global cross-border CRE investment grew more than 12% in 2025, its first annual increase since 2021, according to Cushman & Wakefield. A 2026 Knight Frank survey cited by Commercial Observer found global investors preparing to deploy close to $150 billion into the asset class, with two-thirds prioritizing acquisitions. The wave is forming. The question for operators is whether their onboarding and underwriting can move at the speed the capital now expects.

Why U.S. CRE remains the default destination

The United States is still the deepest, most liquid, and most legally predictable commercial real estate market in the world. For sovereign funds, family offices, and offshore institutions, it offers dollar-denominated yield, transparent title systems, and — critically — an exit market that actually functions when it is time to sell.

The scale of that pull is consistent over time. Invesco Real Estate, drawing on MSCI data, puts long-run average inbound cross-border investment into U.S. CRE near $50 billion a year. Even so, foreign buyers represented only about 11% of all U.S. CRE purchased between 2015 and 2024 — a reminder that the ceiling on foreign participation has historically been operational friction, not demand.

KYC and AML: the bottleneck, then the enabler

Know-Your-Customer and Anti-Money-Laundering checks have long been the slowest, most manual stage of onboarding foreign capital. A single cross-border investor with a layered ownership structure could take weeks to clear. Automated identity verification, sanctions screening, and beneficial-ownership tracing now compress much of that timeline from weeks toward hours — while producing a cleaner, time-stamped audit trail than any manual file.

The efficiency is measurable. Providers of automated KYC report onboarding-time reductions well above 40% after adoption, and industry analyses project that the majority of KYC onboarding is now automated through digital identity and biometric verification. The point is not that machines replace judgment — they don’t — but that they remove the non-judgmental work so analysts can focus on the cases that actually warrant a human.

Automation does not lower the compliance bar. It raises it. A machine checks every name against every list, every time, and documents the result in a form that survives regulatory scrutiny. Done right, the fastest onboarding is also the most defensible.

Where automation still needs a human

It is worth being honest about the limits. Straight-through automation works best in lower-complexity flows; corporate and cross-border onboarding still slows around legal-entity complexity, registry gaps, and opaque control structures. The mature approach pairs AI-driven screening and alert-ranking with human review on ambiguous matches — speed where the data is clean, scrutiny where it isn’t. That blend is the standard serious platforms are building toward.

AI-driven fraud detection where it counts

Cross-border transactions concentrate fraud risk: layered ownership, unfamiliar counterparties, and document sets in multiple languages and formats. This is precisely where AI pattern detection earns its place — flagging inconsistent ownership chains, mismatched funding sources, or structures that resemble known laundering typologies that a tired human reviewer might wave through.

Modern systems lean on graph-based analysis to surface indirect ownership through shell companies and natural-language processing to cut false matches during sanctions screening. The result is a system that moves fast on legitimate capital and slows down exactly where it should: on the small set of transactions that warrant a closer look.

One compliant front door

The advantage compounds when KYC, AML, and fraud detection run inside the same platform that underwrites the asset. Instead of stitching a chain of vendors together, foreign capital can enter U.S. CRE through a single, compliant front door — onboarding, valuation, and risk assessment connected rather than siloed.

That is how CR Equity AI approaches cross-border flow: as an engineering problem with a compliance answer, not a compliance problem that engineering ignores. The platform brings valuation, compliance, and capital markets into one intelligence layer, so a vetted offshore investor and the asset they are funding are evaluated against the same connected system.

Key takeaways

-

Cross-border CRE investment turned a corner in 2025, growing 12%+ for the first time since 2021, with ~$150B of global capital cued up for 2026.

-

The U.S. draws roughly $50B/year in inbound CRE capital on average, yet foreign buyers were only ~11% of purchases (2015–2024) — friction, not appetite, set the ceiling.

-

KYC/AML automation cuts onboarding from weeks toward hours and reduces verification time by 40%+ while strengthening the audit trail.

-

Corporate and cross-border onboarding still needs human review on complex ownership — the best systems blend automation with expert judgment.

-

Running onboarding, fraud detection, and underwriting on one platform gives foreign capital a single compliant entry point.

Global capital is re-engaging with U.S. commercial real estate, and the operators who capture it will be the ones whose compliance moves as fast as their deals. To see how CR Equity AI onboards cross-border capital and underwrites the asset on one connected platform, request a walkthrough at crequity.ai or contact the team at support@crequity.ai.

Sources

-

Cushman & Wakefield — Cross-Border Capital and CRE: Early 2026 Signals — https://www.cushmanwakefield.com/en/insights/cross-border-capital-and-cre

-

Commercial Observer — Foreign Capital Rethinks U.S. Commercial Real Estate — https://commercialobserver.com/2026/02/foreign-commercial-real-estate-capital-trump-2026/

-

Invesco Real Estate — Cross-Border Capital Investment Across Global CRE Markets — https://www.invesco.com/apac/en/institutional/insights/alternative/cross-border-capital-investment-across-global-commercial-real-estate-markets.html

-

Moody’s — AML in 2025: How AI, Real-Time Monitoring, and Global Regulation Are Transforming Compliance — https://www.moodys.com/web/en/us/kyc/resources/insights/aml-in-2025.html

-

KYC-Chain — AI Compliance Agents for KYC/AML in 2026: Hype vs. Reality — https://kyc-chain.com/ai-compliance-agents-kyc-aml/