6 min read

For three decades, commercial real estate due diligence has looked the same: a data room full of PDFs, a spreadsheet, and an analyst working late to reconcile them. That model is ending. Not because PDFs disappeared, but because the records underneath them became directly accessible as structured, queryable data.

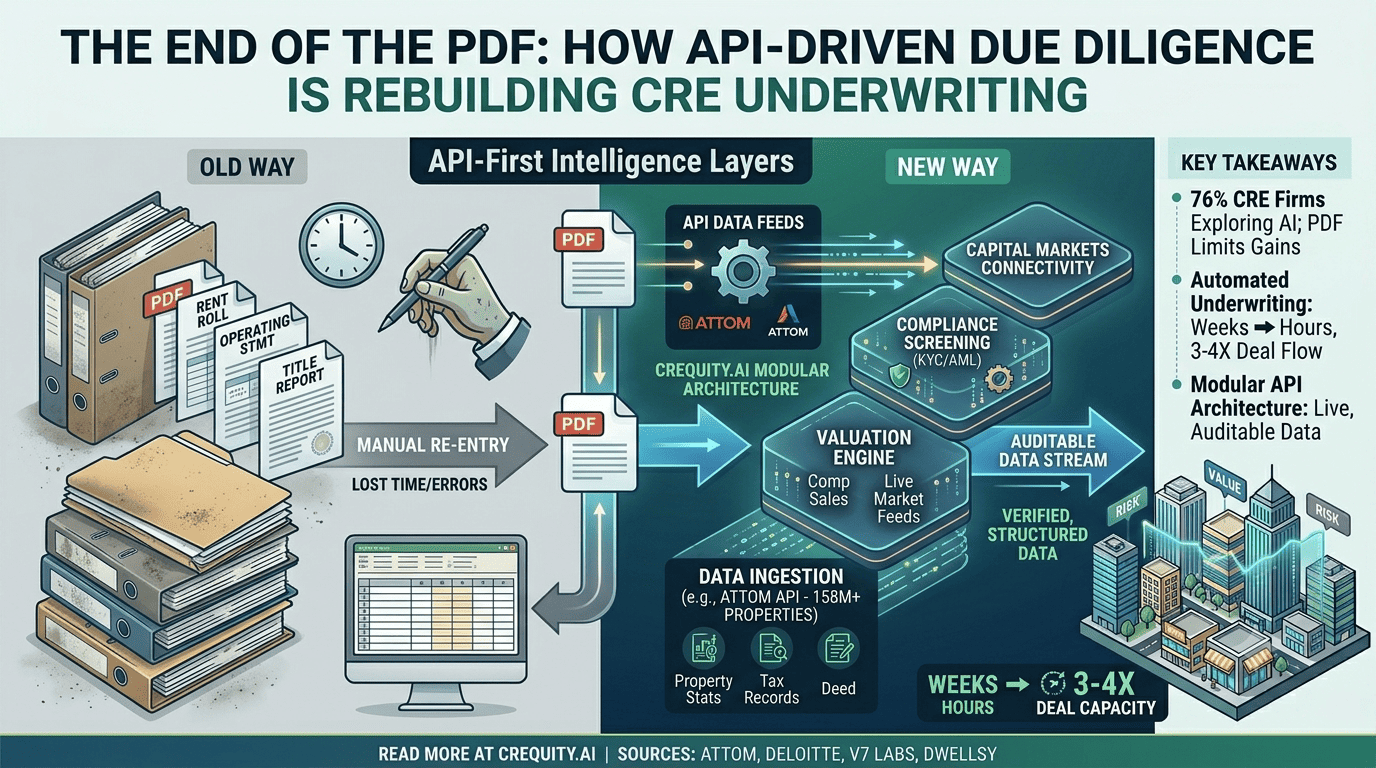

The shift matters because the appetite for AI in CRE has already arrived. Deloitte’s Commercial Real Estate Outlook found that 76% of CRE firms were already exploring or implementing AI, and industry analyses report that automated underwriting can cut loan processing from weeks to hours while letting the same team evaluate three to four times as many deals. The bottleneck holding those gains back is the format the data still arrives in.

A PDF is a photograph of data

A PDF is a picture of information, not the information itself. Every rent roll, operating statement, and title report that lands as a PDF has to be re-keyed, reconciled, and verified by hand. That re-entry is where errors creep in and where days quietly disappear.

The format was reasonable when the alternative was paper. It is an indefensible bottleneck now that the underlying records — ownership, tax history, transactions, valuation — are available through structured data feeds. When a deal’s inputs have to be transcribed before they can be analyzed, the analyst spends their best hours on data assembly instead of judgment, which is where the value has always been.

What API-driven underwriting actually changes

Modern due diligence pulls data directly from source systems through APIs: property characteristics, ownership history, tax records, comparable sales, and title status arriving as structured, machine-readable data. Underwriting that once began with manual entry now begins with a verified dataset already loaded into the model.

The data foundation for this is real and at scale. ATTOM, one of the most widely used property-data providers, delivers structured intelligence across more than 158 million U.S. properties — tax, deed, mortgage, foreclosure, valuation, hazard, and neighborhood data in a single feed. Lenders increasingly describe this kind of feed not as a lookup tool but as core lending infrastructure, pulling live data at the moment a loan is submitted rather than days later.

This is not an incremental gain. When the inputs are clean and verified from the start, the analyst’s time shifts entirely toward the parts of the deal that require human judgment — structure, risk, and pricing.

Modular architecture, not a monolith

How a platform is built determines whether digital due diligence holds up under real conditions. CR Equity AI is designed as a set of composable modules rather than one rigid system: data ingestion, valuation, compliance screening, and capital-markets connectivity each operate as discrete services linked through internal APIs, with integrations into property-data and title sources feeding the underwriting engine directly.

Modularity matters for two practical reasons. The platform can improve one component at a time without a full rebuild, and a client can adopt the specific pieces that fit their existing stack rather than ripping everything out. A fund can plug valuation into its current workflow today and add compliance or capital-markets connectivity when it is ready.

An auditable data layer, not a folder of documents

The endpoint of this shift is a due-diligence process that is faster, more accurate, and fully auditable. Every data point traces back to its source. Every valuation can be reconstructed on demand. When a lender, an auditor, or an investment committee asks how a number was reached, the answer is a complete record rather than an analyst’s recollection.

That auditability is becoming a requirement, not a nicety. As LPs press for audit-ready documentation and regulators tighten expectations on valuation methodology, the data room of the future is not a folder of files — it is a live, verified data layer that the whole transaction is built on.

Key takeaways

-

76% of CRE firms are already exploring or implementing AI, but the PDF data room caps the gains.

-

PDFs force manual re-keying — the source of both errors and lost time in underwriting.

-

API-driven underwriting starts with verified, structured data; providers like ATTOM cover 158M+ U.S. properties in one feed.

-

Automated underwriting can compress loan processing from weeks to hours and multiply deal capacity 3–4x.

-

A modular, API-based architecture lets firms adopt valuation, compliance, or capital markets piece by piece — and keeps every figure auditable to its source.

The data underneath your deals is already structured and live; the only question is whether your underwriting is built to use it. To see how CR Equity AI turns verified data feeds into auditable valuations on a modular platform, request a walkthrough at crequity.ai or contact the team at support@crequity.ai.

Sources

-

ATTOM — Property Data API for Mortgage Lenders — https://www.attomdata.com/news/company-news/data-solutions/property-data-api-for-mortgage-lenders-better-data-for-underwriting-appraisal-review-and-loan-risk/

-

ATTOM — The ATTOM API: Real-Time Property Intelligence — https://www.attomdata.com/news/company-news/data-solutions/the-attom-api-reliable-real-time-property-intelligence-for-developers-and-data-teams/

-

V7 Labs — AI in Commercial Real Estate Investment: A Complete Guide — https://www.v7labs.com/blog/ai-in-cre-investment

-

Dwellsy IQ — Top 15 Real Estate Data Providers (2026 Guide) — https://blog.iq.dwellsy.com/top-15-real-estate-data-providers-2026-guide/